They promise instant approvals, zero paperwork, and rock-bottom fees. Then, three months later, your funds are frozen, your merchant account is terminated, and your customers are filing chargebacks. The offshore payment processing industry has a dirty secret — and this article exposes it completely.

The Offshore Promise vs. The Offshore Reality

When you operate a high-risk business, whether in iGaming, adult content, nutraceuticals, forex, CBD, or subscription services, the mainstream acquiring world slams the door in your face. That's when the offshore brokers show up, perfectly timed, with their glossy pitch decks and whispered promises.

It sounds irresistible: get approved in 48 hours, pay low processing fees, no compliance headaches. But what they're actually selling you is instability dressed up as opportunity. Every single one of those benefits has a catastrophic hidden cost that reveals itself at the worst possible moment.

Understanding how Visa and Mastercard rules specifically impact high-risk merchants is essential before you sign anything with any processor, onshore or offshore.

"The cheapest payment processor is never the one with the lowest rate. It's the one that doesn't freeze your funds at the worst possible moment."

The 7 Deadliest Disadvantages of Offshore Payment Processing

No Regulatory Oversight — You Have Zero Legal Protection

Offshore processors typically operate from jurisdictions such as Seychelles, Vanuatu, or Belize — territories with minimal or non-existent financial regulation. If your funds disappear, there is no Financial Conduct Authority, no Banco de España, no BaFin to call. You have no legal recourse. You simply lost your money.

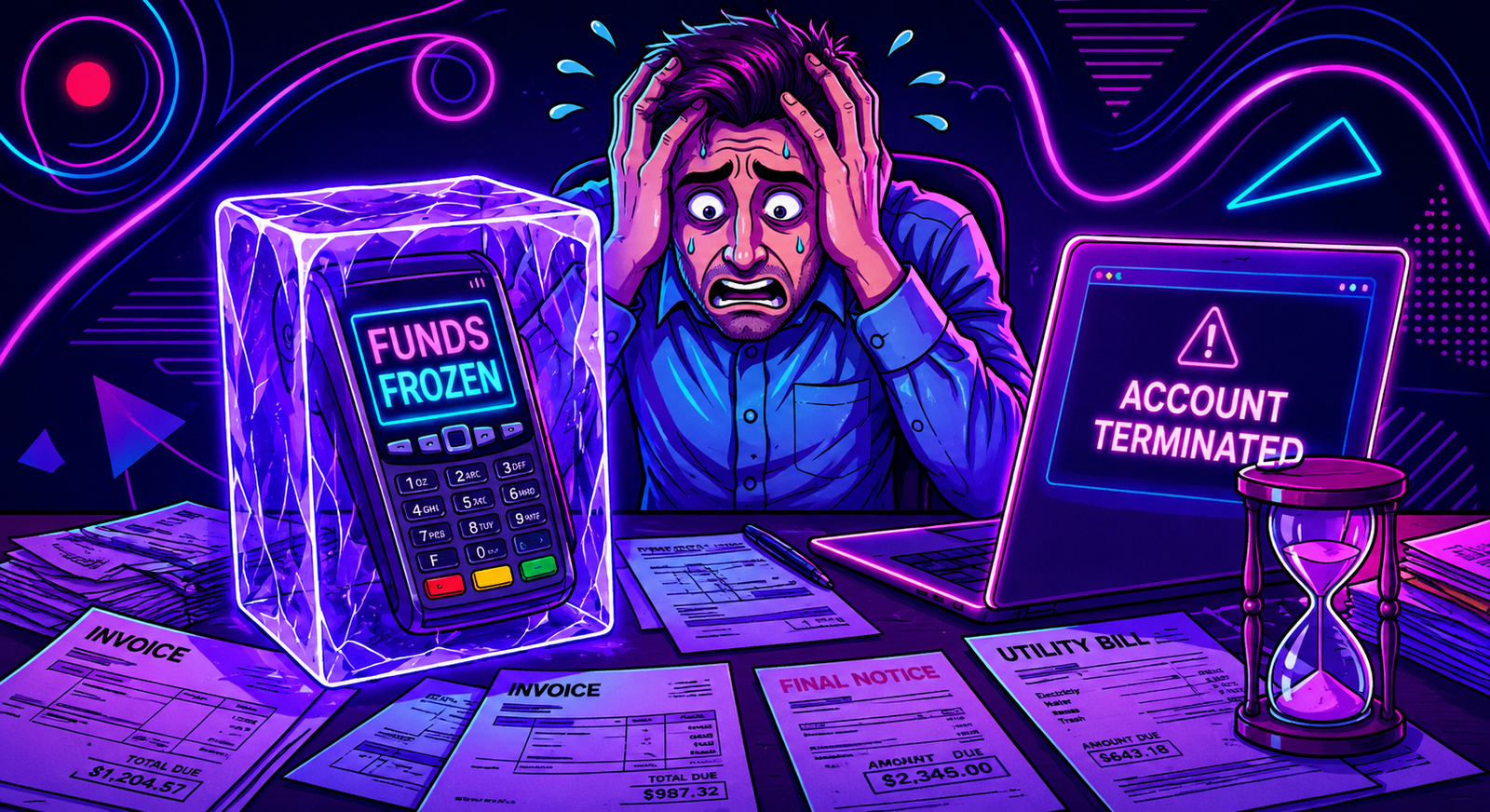

Fund Freezing and Rolling Reserves That Destroy Your Cash Flow

Offshore processors routinely hold 5–15% of your monthly volume in "rolling reserves" for 90–180 days. On a business processing €200,000 per month, that's €30,000 locked away every single month. Then, when they decide to terminate your account without warning and without cause, they can hold your reserve for up to 6 months. Businesses have collapsed waiting for that money.

Sudden Account Termination — No Warning, No Explanation

Offshore merchant accounts are notoriously unstable. A chargeback ratio spike, a risk team audit, a Visa or Mastercard network flag — any of these can trigger an immediate termination. Your payment page stops working on a Tuesday afternoon. Your customers can't check out. You lose tens of thousands in revenue while you scramble for an alternative. This is not hypothetical. This happens daily.

The reality behind offshore payment processing: frozen funds, sudden terminations, and zero recourse.

MATCH List Placement — A Five-Year Industry Ban

When an offshore processor terminates your account due to excessive chargebacks or fraud, they may report you to the Mastercard MATCH (Member Alert to Control High-Risk Merchants) list. Once you're on it, virtually no legitimate acquiring bank in Europe, North America, or Australia will onboard you. This blacklist lasts five years. Your offshore "easy approval" just became a five-year death sentence for your payment infrastructure.

Hidden Fees That Multiply Your True Processing Cost

That "2.5% flat rate" an offshore processor advertises? By the time you add currency conversion markups, cross-border fees, chargeback fees (€35–€100 each), monthly minimum fees, PCI compliance fees, and termination fees, your effective rate can reach 6–9%. A licensed European acquirer charging 3.5% with full transparency is cheaper in every real-world scenario. The topic of what your processor isn't telling you about fees deserves its own deep-dive — the hidden cost structure is genuinely alarming.

Non-Compliance With PSD2, GDPR, and 3DS2 Requirements

European customers transacting through non-PSD2-compliant processors are exposed to regulatory violations that could implicate your own business directly. If your payment page doesn't support proper Strong Customer Authentication via 3DS2, you face elevated fraud rates, increased chargebacks, and potential liability under EU data protection law. Most offshore processors simply don't meet these standards. Visa's published rules and Mastercard's compliance framework both make these obligations explicit — your processor must meet them.

Reputational Damage That Destroys Customer Trust

Customers increasingly notice when a payment page redirects through an obscure third-party domain registered in Belize. Conversion rates drop. Trust signals evaporate. Your brand, which you spent years building, takes a hit every time someone sees an unfamiliar processor name on their bank statement, or worse, a disputed charge they can't resolve because the processor has no customer support infrastructure.

Quick question before you read on

Is your current processor actually licensed in Europe?

If you're not 100% sure of the answer, it takes about 90 seconds to start the conversation with our team. We'll tell you honestly what your options are.

Check My Eligibility — It's Free ↗You pay nothing unless approved.

The Anatomy of an Offshore Payment Processor Collapse

Not every offshore processor is running a deliberate scam — but the structural incentives of the offshore model create predictable failure patterns that harm merchants regardless of intent. Here's how it typically unfolds.

Phase 1: The Seduction

A slick ISO broker contacts you, often through LinkedIn or a fintech forum. They offer fast approval, low rates, and no problem with your business type. The contract is 40 pages of legalese that includes clauses allowing account termination without cause and fund holds for up to 180 days. You sign because you're desperate to start processing.

Phase 2: The Honeymoon

Processing works. Settlement arrives, mostly on time. You scale your marketing. Monthly volume grows to €100k, €200k, €500k. You stop worrying about the processor. This is exactly what they want, because the more volume running through the account, the more reserve they accumulate on your behalf.

Phase 3: The Collapse

A chargeback spike hits. The processor's risk team flags your account. Without a single email warning, your merchant ID is terminated. Your checkout page returns errors. Customers can't pay. Your reserve, potentially six figures, is frozen. The support team stops responding. You can read exactly why payment gateways freeze funds and what you can realistically do about it — the answer is usually "very little, after the fact."

Offshore vs. Licensed European Acquirer — A Direct Comparison

Why Ireowo Only Works With Licensed European Acquiring Banks

At Ireowo, we are not the cheapest option in the market. We never will be, and we are proud of that. The merchants who come to us have usually lived through at least one offshore disaster. They've had their funds frozen. They've lost customers during a critical sales period because their checkout stopped working. They've spent 90 days on hold with a support team in a timezone they can't reach.

We work exclusively as a broker and ISO with acquiring banks that hold full banking licences within the European Economic Area. These are regulated institutions subject to EBA oversight, Visa and Mastercard network rules, and national banking authority supervision. When you process with one of our partner banks, you are processing with an institution that has something significant at stake: its licence. That accountability changes everything about how your account is managed.

Our goal is to help you secure stable, long-term processing accounts with tier-one institutions — not the fastest approval, not the lowest teaser rate, but the most secure and sustainable payment infrastructure your business can build on.

What "Licensed in Europe" Actually Means for Your Business

A bank with a European banking licence operates under directives including PSD2, the EU Anti-Money Laundering framework (AMLD5 and AMLD6), and GDPR. They are subject to regular audits, capital adequacy requirements, and consumer protection obligations. Their agreements with Visa and Mastercard are direct principal-level relationships, not daisy-chain subprocessor arrangements that can collapse without warning.

When your acquiring bank is licensed in Europe, your merchant agreement is legally enforceable in a jurisdiction with mature contract law. If something goes wrong, you have options. That is not a luxury — that is the foundation of a serious business. It is also worth understanding how transaction laundering rules affect high-risk merchants, since offshore processors often place merchants in compliance exposure zones without any warning. Understanding Visa's acceptance credentials and standards helps clarify what a legitimate acquiring relationship actually looks like.

Ireowo connects high-risk merchants with fully licensed European acquiring banks — stability and compliance built in from day one.

Red Flags: How to Identify a Problematic Processor Before You Sign

Protecting yourself starts with knowing what to look for. Here are the definitive warning signs that you are dealing with an unlicensed or structurally risky payment processor.

🚩 Red Flag 01 — The contract contains termination-without-cause clauses

Read every contract before signing. If the termination section allows them to close your account without explanation and hold reserves for 180 days, that clause was written to protect them, not you. This is one of the most common weapons used against merchants by offshore processors.

🚩 Red Flag 02 — Their website was registered less than two years ago

The offshore processor market is full of pop-up operations. Check the domain registration date on WHOIS. If the company presenting itself as a major payment infrastructure player launched its website 14 months ago, that is a serious concern that due diligence cannot overlook.

🚩 Red Flag 03 — They promise approval in under 72 hours for high-risk categories

A genuine underwriting review for a high-risk merchant account takes time. Compliance teams review your business model, your chargeback history, your website, your corporate documents, and your bank statements. If someone promises you approval before they've seen any of that, they are not doing proper due diligence — and that will eventually cost you everything.

🚩 Red Flag 04 — No verifiable licensing information available

Every legitimate acquiring bank in Europe can be verified on the European Banking Authority register at eba.europa.eu. Check it. If your processor cannot demonstrate a licence-holding partner that appears on that register, you are operating outside the regulatory perimeter entirely and carrying all of that risk yourself.

🚩 Red Flag 05 — Vague answers about who actually holds your funds

Any legitimate payment solution can tell you which licensed institution holds your funds. If an ISO or broker gives you a vague answer like "we have multiple banking relationships," or deflects the question entirely, walk away. You deserve to know who holds your money, full stop.

Ireowo Payment Solutions

Your High-Risk Business Deserves a Real Banking Partner

Submit your pre-application today. Our team reviews every case personally and connects you only with acquiring banks that are the right fit for your business category and volume. No upfront fees, no empty promises.

Start Processing Payments Securely — Apply Now ↗You pay nothing unless approved.

Curious Things You're Probably Wondering

If offshore processing is so dangerous, why do so many businesses still use it?

Because the alternative — getting rejected by every mainstream bank — feels worse. High-risk merchants are often under pressure, and that pressure is exactly what offshore brokers exploit. Many businesses don't realize what they've signed until the account is terminated and their money is frozen. By then, the offshore processor has already collected months of reserve funds and processing fees. The desperation cycle is very real, and very deliberate on their part.

Can I get my frozen funds back from an offshore processor?

It is very difficult, and the outcome depends almost entirely on the jurisdiction where the processor is registered. In most offshore jurisdictions — Seychelles, Vanuatu, St. Vincent — there is no effective legal mechanism to compel fund release. Some merchants have succeeded through international arbitration or by engaging a specialized fintech lawyer, but the process is expensive and the success rate is low. This is precisely why prevention, choosing a licensed EU acquirer from the start, is so critical.

Does Ireowo work with businesses that have been placed on the MATCH list?

MATCH list placement makes European acquisition significantly harder, but not always impossible. Each case depends on the reason for placement, how long ago it occurred, and what remediation steps the merchant has taken since. We review every situation individually and give you an honest assessment of what's achievable before you invest time in an application. We will never promise you something we cannot deliver.

How much more expensive is a licensed European acquirer compared to an offshore one?

In raw headline rates, a licensed EU acquirer may appear 0.5–1.5% more expensive than an offshore quote. But when you factor in hidden fees, FX conversion markups, chargeback penalties, rolling reserve opportunity costs, and the catastrophic revenue loss from a sudden account termination, a licensed European acquirer is almost always cheaper over a 12-month horizon. We can model this specifically for your business volume — just mention it when you apply.

What types of businesses does Ireowo actually work with?

We specialize in high-risk merchant categories that have legitimate, compliant business models but face difficulty securing processing through conventional channels. This includes iGaming and online gaming, adult entertainment, nutraceuticals and supplements, forex and CFD brokers, cryptocurrency-related services, subscription businesses with free-trial models, travel and timeshare, and certain e-commerce verticals with elevated chargeback exposure. If your business operates legally in its target market, we want to hear from you.

What does "You pay nothing unless approved" actually mean?

It means exactly what it says. Ireowo does not charge application fees, setup fees, or consultation fees. Our compensation comes from a revenue-share arrangement with the acquiring bank, and that only activates once you are approved and actively processing. If we cannot get you approved with a licensed EU acquirer, you owe us nothing. We believe that is the only ethical way to operate as a broker in this industry.

How long does the application process take with a licensed European acquirer?

A genuine, compliant underwriting process for a high-risk merchant account typically takes 2–6 weeks. The timeline depends on the completeness of your documentation, the business category, and current processing volumes at the acquiring bank. We manage the entire process on your behalf, guide you through document requirements, and maintain active communication with the underwriting team throughout. Faster is not always better when the alternative is skipping proper due diligence entirely.