In the world of online payment processing, transparency is a rare commodity. Many businesses discover what card processing really costs them only when the first settlement hits and the numbers are nothing like what they imagined. If your company has been classified as high risk, the question that keeps you up at night is entirely justified: how much is this actually going to cost me?

This article breaks it down with zero fluff. No vague percentages, no buried asterisks. Just the real structure of high-risk payment processing fees so you can run your numbers with confidence and pick the right partner from day one.

The Reality of Risk Categories: Low, Medium, and High

Before we get to the numbers, you need to understand how acquiring banks actually sort merchants. Contrary to popular belief, the three tiers are not simply a reflection of how sketchy your business is.

Traditional brick-and-mortar retail. Minimal fraud exposure. Simple onboarding, lowest MDR rates.

An informal category for merchants who don't clearly fit either extreme. Banks apply high-risk precautions regardless.

Determined largely by MCC code, not your chargeback history. Strict onboarding, rolling reserve, and higher fees apply.

Low Risk: The Baseline

Low-risk merchants are typically traditional retailers with physical storefronts, where in-person card verification keeps fraud rates minimal. These businesses enjoy the leanest fee structures the industry offers.

High Risk: It's About the MCC, Not the Morality

This is the part most merchants get wrong. Being classified as high risk today does not necessarily mean you have a high chargeback ratio or a problematic history. In the vast majority of cases, your classification is determined strictly by your Merchant Category Code (MCC), a four-digit code assigned according to card network rules. You can review the official Visa Rules and Mastercard Rules to understand how card brands define and govern merchant categories.

If you want a deeper explanation of exactly why your business landed in this category, we cover the full picture in our article on Visa and Mastercard rules for high-risk merchants, which walks through the specific MCC codes and card scheme policies that trigger this classification.

Medium Risk: The Unofficial Third Tier

There is an informal middle ground for companies that sit on the edge. They do not perfectly match the definition of a low-risk retailer, but their MCC is not explicitly listed as high risk either. From a practical standpoint, acquiring banks apply the same caution and precautions to these merchants as they do to high-risk accounts. The pricing reflects that reality.

What Should You Expect as a High-Risk Merchant?

Two things happen immediately when an acquiring bank flags your business as high risk. First, onboarding becomes significantly slower and more demanding. You will submit more documentation, undergo more scrutiny, and wait longer for approval. Second, and most directly relevant to your bottom line, the price goes up.

The good news is that the exact rate you land at within the 2%–7% range depends heavily on your volume and your processing history. New merchants with no track record start toward the higher end. Established businesses with clean chargeback ratios and strong monthly volume have real leverage to negotiate toward the lower end.

If you are already processing and you have experienced frozen funds or sudden account terminations, understanding the full fee picture is only part of the problem. Our guide on why payment gateways freeze merchant funds explains the other side of the risk equation that most processors never explain upfront.

Tired of discovering hidden fees after the fact?

You pay nothing unless approved.

Start processing payments for your high-risk businessThe Four Cost Blocks Every High-Risk Merchant Must Understand

Your total cost to process a payment is not a single number. It is the sum of four distinct layers, each charged by a different party in the chain. Here is how to read your statement like a pro.

1. Bank and Acquiring Fees: The IC++ Model Explained

The most transparent pricing structure in the payments industry is IC++ (Interchange Plus Plus). Under this model, you pay three components stacked on top of each other: the interchange fee, a card scheme assessment fee, and the acquirer's margin. Nothing is blended or hidden.

What is the Interchange Fee (IC)?

The IC is the fee paid directly to the cardholder's issuing bank every time a transaction is processed. It compensates the issuing bank for the credit risk it takes, for running its rewards programs, and for covering its operational costs. This rate is not negotiable and is set by the card networks. You can see the current published rates at the Mastercard interchange rates page and the equivalent Visa fee schedules.

The IC rate can swing between 0.10% and 1.5% or higher depending on:

- Card type (debit vs. credit vs. corporate card)

- Geography of the card (European consumer debit cards are capped at 0.20% by EU regulation, but corporate cards or cards issued outside Europe carry significantly higher rates)

- Transaction method (card-present vs. card-not-present)

- Your own MCC code

On top of the IC, the acquirer adds their own commercial margin. For high-risk merchants, this combined MDR (Merchant Discount Rate) typically sits between IC++ 2% and IC++ 7%. The acquirer sets this number after reviewing your processing volume, chargeback history, refund ratios, and fraud reports. The cleaner your track record and the higher your monthly volume, the better your negotiating position.

2. The Rolling Reserve

If there is one clause in your merchant agreement that surprises high-risk merchants most, it is the Rolling Reserve. This is not an optional add-on. It is an industry-wide standard for every high-risk merchant account, full stop.

The mechanics work on a rolling basis. After 180 days, the reserve funds from your early transactions begin releasing back to you continuously, as long as your account remains active and in good standing. It creates a temporary cash-flow impact, particularly in your first six months of processing, but it is entirely recoverable capital.

Some acquirers will negotiate the reserve percentage down to 5%–8% for merchants with demonstrable history or substantial volume commitments. Always ask. It is one of the most impactful negotiating points in your entire agreement.

3. Operational Fees: Chargebacks, Payouts, and Authorizations

Beyond the MDR and the rolling reserve, your merchant account will generate a set of per-event fees throughout its lifecycle. These are predictable costs, and once you know them, you can factor them into your unit economics accurately.

| Fee Type | Typical Range | When It Applies |

|---|---|---|

| Chargeback Fee | €18 – €50 per dispute | Each time a cardholder opens a dispute or chargeback against your business |

| Payout (Settlement) Fee | €5 SEPA / €25 SWIFT | Each time the acquirer transfers your settled funds to your bank account |

| Authorization Fee | €0.10 – €0.25 per attempt | Every authorization request sent to the issuing bank, whether approved or declined |

A note on chargebacks specifically: beyond the per-dispute fee, there are card scheme monitoring programs that can impose additional fines if your chargeback ratio exceeds defined thresholds. Mastercard's dispute management framework and Visa's equivalent programs set clear ratio limits, and exceeding them can result in escalating monthly fines and, ultimately, account termination. For a full breakdown of what the card networks actually expect from you, read our article on what your processor isn't telling you about high-risk transparency.

4. Payment Gateway Technical Fees

The acquiring bank handles the financial settlement. The payment gateway handles the technology that connects your website or platform to that bank. These are two separate cost centers, and both appear on your monthly statement.

| Fee Type | Typical Range | Notes |

|---|---|---|

| Transaction Fee | €0.20 – €0.50 per transaction | Applies to both successful and declined transactions |

| Refund Fee | €0.20 – €1.00 per refund | Charged when you initiate a voluntary return to a customer |

The transaction fee from the gateway is charged per attempt, not per approval. If your authorization rate is low, those declined transaction fees accumulate quickly and are easy to overlook when modeling your cost of acceptance. Factor them in.

Annual Card Scheme Registration Fees

This is the cost block that almost no one mentions during sales calls, yet it is mandatory for a specific subset of high-risk merchants. If your business falls under a tightly regulated MCC according to Visa and Mastercard policy (online pharmacies, gambling, adult entertainment, and similar verticals), you are legally required to register with each card scheme and pay an annual program fee to operate.

Visa MARP (Merchant Alert to Control High-Risk) program: approximately €900 per year.

Mastercard equivalent program: approximately €500 per year.

These fees are non-negotiable and non-refundable. They are paid directly to the card networks, not to your acquirer or gateway. If you operate in one of these verticals and your processor has not mentioned this requirement, that is a serious gap in their guidance. You can review the official acceptance criteria at the Visa acceptance solutions portal.

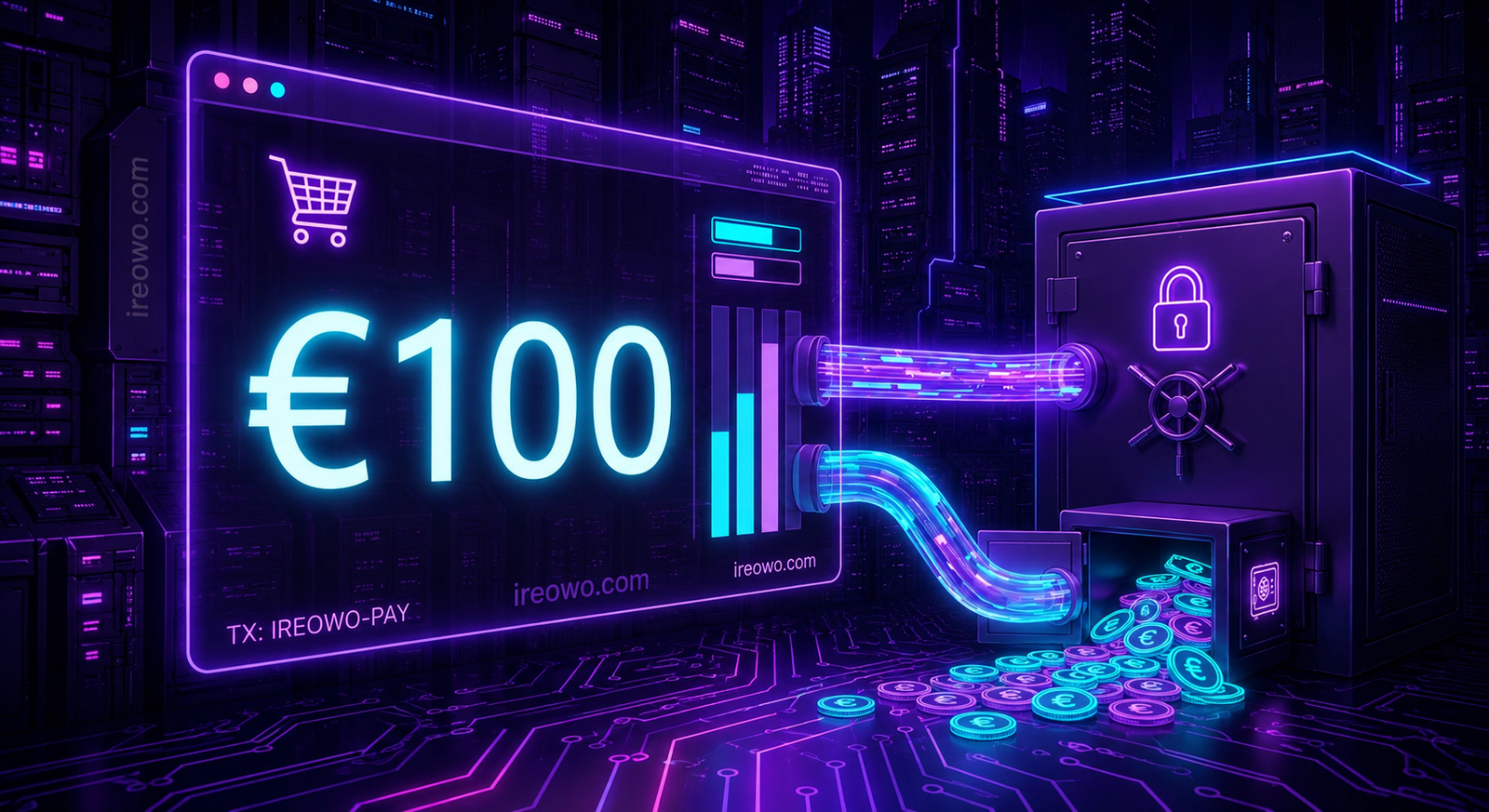

Practical Example: What Hits Your Account on a €100 Sale?

Theory is useful. Numbers are better. Here is the exact breakdown of a single €100 online transaction, using a typical high-risk merchant profile with an agreed MDR of IC++ 5% and a standard 10% rolling reserve at 180 days.

Of that €100 sale, €5.40 leaves immediately in direct fees. Another €10.00 is temporarily held and returned to you after 180 days. You receive €84.60 in your next payout. The payout fee itself (€5 SEPA or €25 SWIFT) is spread across all the transactions settled in that batch, so it becomes negligible at scale but is worth tracking at lower volumes.

Note: This article focuses exclusively on online card payment processing. It does not include the costs of physical POS terminals or in-store card readers, which follow a different fee structure entirely.

Why You Should Always Work With Licensed European Acquiring Banks

The fee structures we have outlined represent the legitimate industry standard. Yes, you will encounter offers that seem dramatically cheaper. Someone will promise you IC++ 1% with no rolling reserve and instant approval. In the high-risk space, those promises are the most expensive offers you will ever receive, paid not in fees but in frozen accounts, seized balances, and terminated processing right when your business needs it most.

There is a specific and dangerous practice that some unregulated operators use called transaction laundering, where your transactions are routed through mismatched merchant accounts to disguise their nature. It feels seamless until Visa or Mastercard discovers it, at which point your funds are frozen and your business is blacklisted. Our detailed breakdown of transaction laundering risks for high-risk merchants explains exactly how this happens and why it destroys businesses that never even knew they were doing anything wrong.

Conclusion: Know Your Numbers Before You Sign Anything

Understanding the true cost of accepting card payments is not optional for a high-risk business. It is the foundation of your margin calculations, your cash flow forecasting, and your ability to scale sustainably. The five cost blocks covered here, namely the MDR, the rolling reserve, the operational fees, the gateway fees, and the card scheme registration, are all predictable, manageable, and negotiable to varying degrees. The one thing that is not manageable is discovering them after you have already committed to a bad contract.

As the saying goes in business: clear accounts preserve friendships. And in payments, clear accounts preserve businesses.

Ready for a payment processing account that shows you every number upfront?

Stable processing. No sudden freezes. 100% transparent fees from licensed European acquirers.

You pay nothing unless approved.

Apply for Your High-Risk Payment Gateway Now →Curious Things You're Probably Wondering

If my rolling reserve is 10% for 180 days, does that money earn interest while it sits there?

Almost universally, no. The rolling reserve is held in a non-interest-bearing account controlled by the acquiring bank. The bank benefits from holding your capital, but you do not earn a return on it. The reserve exists purely as a risk buffer for the acquirer, not as an investment vehicle for you. This is standard practice across the industry and is one of the reasons that negotiating the reserve percentage down (rather than accepting the default 10%) has a real financial impact on your business from day one.

Can I get a high-risk merchant account if I have never processed payments before and have no history?

Yes, but expect the least favorable terms. Without a processing history, acquirers have no data to assess your chargeback risk, fraud patterns, or refund ratios. They compensate for that uncertainty with higher MDR rates, a higher rolling reserve percentage, and sometimes a cap on your monthly processing volume until you build a track record. Starting at IC++ 5%–7% with a 10%–15% reserve is not unusual for new high-risk merchants. As you accumulate six to twelve months of clean processing history, you gain real leverage to renegotiate.

What happens if my chargeback ratio goes above the card network thresholds?

Two things happen, and neither is pleasant. First, the card networks (Visa and Mastercard) enroll you in a chargeback monitoring program, which comes with monthly fines that escalate the longer you stay in the program. Second, if you do not bring the ratio down within the program's timeframe, the acquiring bank is under pressure from the card networks to terminate your account. The specific thresholds and fine structures are published in the official Visa and Mastercard rules documents. Staying below 1% monthly is the generally accepted target, with anything above 1.5% putting you in active monitoring territory.

Why do I get charged an authorization fee even when a transaction is declined?

Because the authorization request itself costs the network money to process, regardless of the outcome. When a transaction is submitted, the acquirer sends a request to the card network, which forwards it to the issuing bank, which checks the account and responds. That entire routing and processing chain consumes infrastructure whether the answer comes back as an approval or a decline. The acquiring bank passes that cost to you. It is one of the less intuitive fees in the structure, but it is entirely standard. The practical implication is that optimizing your authorization rate (reducing unnecessary declines through better payment routing or retry logic) directly reduces this cost.

Is it legal to pass processing fees on to my customers as a surcharge?

This depends entirely on the jurisdiction your customers are in, not just where your business is registered. In many European countries, surcharging consumer cards is prohibited under the EU Payment Services Directive. In the United States, surcharging rules vary by state and are governed by card network rules that require specific disclosures and caps. In general, if you want to pass costs to customers, the safest and most common approach is to build them into your product pricing across the board rather than applying a visible line-item surcharge at checkout. Always consult with a legal advisor familiar with payments regulation in your specific markets before implementing any surcharge policy.

If a customer disputes a charge and I win the chargeback, do I get the chargeback fee back?

In most cases, no. The chargeback fee (typically €18–€50) is charged by the acquirer to cover the administrative cost of processing the dispute, and that cost is incurred whether you win or lose. Some acquirers have policies that return the fee on successful representments, but this is the exception rather than the rule and is worth asking about explicitly during contract negotiations. Winning a chargeback dispute recovers the transaction amount, which is significant, but the fee itself is usually a sunk cost either way. This is one reason why prevention (through clear billing descriptors, strong customer communication, and solid evidence documentation) is always more economical than cure.

Can I have multiple merchant accounts across different acquirers to spread my risk?

Yes, and for high-volume high-risk merchants this is not just permitted, it is genuinely good strategy. Running two or more merchant accounts with different acquirers gives you redundancy (if one account is suspended, you do not lose all processing capacity), and it can give you geographic coverage advantages (different acquirers may have better authorization rates for specific card-issuing regions). The complexity is that each account requires its own onboarding, its own rolling reserve, and its own compliance management. A broker like Ireowo can help you manage multiple banking relationships from a single operational layer rather than managing each acquirer relationship independently.