Let's be direct about something most payment consultants won't tell you: the offshore company that was supposed to protect your wealth might be quietly killing your revenue. Not because of tax audits or compliance letters, but because Visa and Mastercard have already decided you don't exist in the markets that matter most.

This is the offshore trap. And thousands of otherwise smart entrepreneurs fall into it every year.

The Offshore Dream: What the Pitch Promises You

Everyone knows the appeal of setting up an offshore company We're talking about establishing a legal entity outside the European Union, typically in very low-tax jurisdictions such as Saint Vincent and the Grenadines, the Bahamas, Bermuda, Panama, Curaçao, Anjouan, the Seychelles, Hong Kong, Singapore, the United States (Delaware), or the United Arab Emirates (Dubai).

If we set aside Andorra and Switzerland which, due to geographic proximity and specific bilateral agreements, have managed to integrate reasonably well into the European market ecosystem the rest of the jurisdictions listed above can seem like paradise on paper. They promise enormous tax advantages and, supposedly, total secrecy about what you sell and invoice.

However, that secrecy is running out of time. Thanks to frameworks like the CRS 2.0 (Common Reporting Standard), local tax authorities are increasingly finding out everything anyway. But the real problem is not fiscal at all. The real problem is that by moving offshore, you are actively closing the doors to international commerce, particularly in the most profitable e-commerce markets in the world: the European Union and the United States.

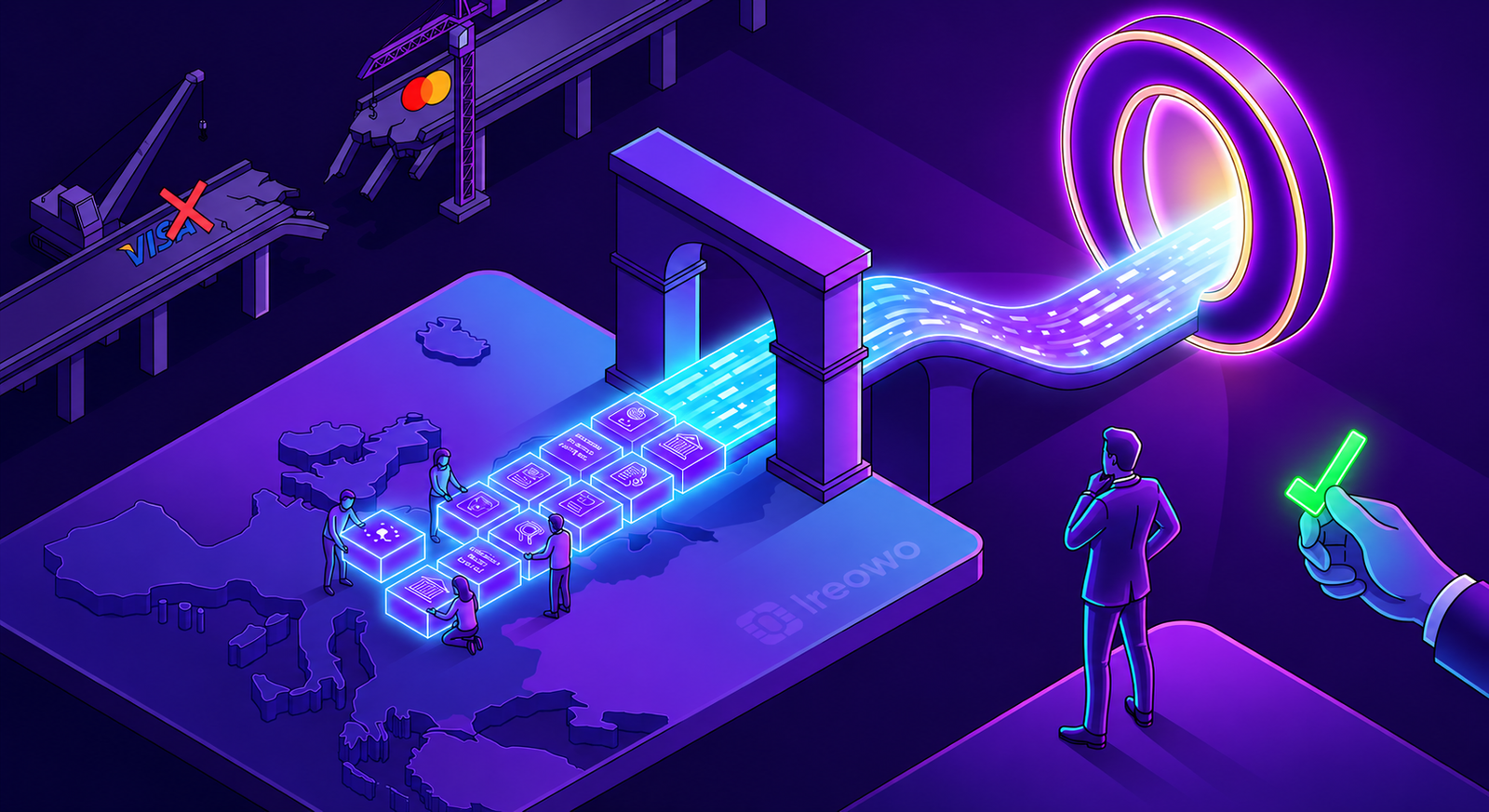

The Visa and Mastercard Wall: No Local Presence, No Payments

Call it recent policy changes or rules that always existed but are now enforced without exception: today, the Cross-Border Acquiring Rules of Visa and Mastercard are unambiguous. They will not approve a merchant account without local representation in the market you want to process.

The United States Case

If you have an LLC in the USA but your director is not a resident in the country, forget about processing payments in a clean, stable, and cost-effective way. The rule is simple and it is applied consistently.

The United Kingdom Case

Exactly the same applies. If you have a British LTD but neither the director nor at least one of the main shareholders is a resident in the UK, you will not be approved by any first-tier acquiring bank. Full stop.

Ireowo European Acquiring Specialists

Does your company meet the requirements but you still can't find a bank that will approve you? We help you open your processing account with 100% licensed and regulated European acquiring banks. No grey zones, no shady intermediaries, and with the certainty that your money is safe.

You pay nothing unless approved.

Start Processing Payments for Your High-Risk Business TodayAsian and Middle Eastern Processing: The Cross-Border Trap

Now imagine your company is registered in Hong Kong or Dubai. The rules force you to find a payment processor based in Asia or the Middle East, since European and American acquirers are prohibited from processing for companies domiciled in those regions.

Let's say you successfully find an Asian processor that allows you to charge customers in Europe or the US. At that point, you fall straight into the Cross-Border transaction trap:

- It is dramatically more expensive. Interchange fees skyrocket the moment a transaction is classified as cross-border, and those costs land directly on your margin.

- Approval rates collapse. European issuing banks do not like seeing charges originating from Asia or Dubai. They will block your legitimate customers' transactions even when those customers have sufficient funds simply because the origin triggers a fraud flag.

The contrast is stark: if your company belongs to the European Union, Switzerland, Andorra, or Monaco, the regulatory environment is far friendlier. All that's needed is for the director or one of the shareholders to reside in any EU member state to operate completely normally within the SEPA zone.

Real Alternatives for Entrepreneurs Outside the EU

If you live in European countries that are not yet part of the Union such as Turkey, Serbia, Ukraine, Moldova, or Georgia or if you are based in Latin America and want to access the European market cleanly, you have two main options:

Option 1: Relocation

If your budget, logistics, and personal situation allow it, legally moving to a European Union country is the most comprehensive solution. It solves the residency requirement at the root level and opens every door simultaneously.

Option 2: Local Corporate Structure (The Smart Move)

There are specialized law firms and corporate service providers that open your company inside the EU and assign you a nominal local director. With this single step, you satisfy the most critical banking requirement. It is fast, it is legal, and it is the approach that serious merchants use when relocation is not immediately viable.

Tax Havens Inside Europe: They Already Exist

What about those who already live within the EU and are looking at offshore structures purely to reduce their tax burden? The answer is that you don't need to leave Europe at all.

There are jurisdictions within the EU with remarkably attractive tax regulations that acquiring banks actively welcome:

Estonia

All profits that you reinvest back into your company are taxed at 0%. The official Estonian e-Residency program makes this structure entirely accessible and fully documented by the government itself. You are not relying on a loophole you are using a deliberate national policy designed to attract entrepreneurial capital.

Cyprus

One of the lowest and most business-friendly corporate tax burdens in all of Europe, with a mature legal infrastructure built for international commerce.

There are hundreds of online agencies that will set up a legitimate company in these jurisdictions without forcing you to gamble on a Delaware LLC or a Dubai free zone entity. And when your business scales, raising investment, expanding operations, and diversifying under a European corporate structure is infinitely simpler than doing the same with a Caribbean offshore.

Conclusion: Cheap Always Costs More in the End

Every euro you think you are saving by going offshore tends to come back multiplied: in legal fees to recover funds frozen by a shadow aggregator, in ongoing compliance costs to keep a grey-zone structure operational, or in lost revenue from declined transactions that your customers gave up on.

We understand that tax pressure in many countries is suffocating. But inside the European Union ecosystem, there are legal, secure, and scalable tools to grow your revenue without putting your cash flow at risk. The choice between a tax-efficient European structure and an offshore trap is not even close once you account for real-world payment processing outcomes.

Protect Your Revenue. Process With Confidence.

If you operate a complex or high-risk business model, you need a payment infrastructure that actually has your back. At Ireowo, we specialize in high-risk payment gateway solutions for companies registered in Europe. Full transparency, direct acquiring relationships, and built-in anti-freeze protection.

You pay nothing unless approved.

Discover Our Solutions and Start Processing SecurelyCurious Things You're Probably Wondering

If my offshore company is legal, why would a bank still refuse to process my payments?

Legality and processability are two completely different things. Your offshore company can be 100% legal under its local jurisdiction and still be rejected by Visa and Mastercard's acquiring networks. The card schemes apply their own Cross-Border Acquiring Rules independently of tax law. If your company does not have a director or principal shareholder residing in the market where you want to process, the acquirer simply cannot approve the merchant account regardless of how legitimate your business actually is.

Can I just use a payment aggregator like Stripe or PayPal to avoid this whole problem?

Stripe, PayPal, and similar platforms operate under the same Visa and Mastercard rules. They also have their own risk models, and high-risk business categories are frequently terminated without warning on these platforms, often with funds held for 90 to 180 days. For any serious volume or any business in a regulated category, a direct acquiring relationship with a licensed European bank is the only infrastructure that provides genuine stability. Aggregators are fine for testing a concept; they are not a foundation.

What exactly is a "shadow aggregator" and how do I recognize one before it's too late?

A shadow aggregator is a payment intermediary that puts your transactions through accounts that do not belong to your business, often without disclosing this to you. The red flags include: unusually high approval rates with no real underwriting process, requests to process under a different business name or category, vague or unverifiable banking relationships, and contracts with no clear regulatory disclosure. If a processor is promising you approvals that every regulated bank declined, that is the clearest warning sign of all. Speak with our team before signing anything you're unsure about.

I live outside the EU. Can I still open a European company and get a real merchant account?

Yes. The residency requirement is about the director or a principal shareholder of the company, not necessarily you personally, as long as the corporate structure is set up correctly. Specialized corporate service providers can assign a nominal EU-resident director to your company, satisfying the banking requirement. This is a completely standard and legal practice, used by thousands of international merchants who operate legitimately in the European market. Once the structure is in place, Ireowo can connect you with the right licensed acquiring bank for your business category.

Is Estonia's 0% reinvestment tax actually real, or is it a gimmick?

It is real and it is documented by the Estonian government itself. The Estonian corporate tax system only applies tax at the point of profit distribution. If you reinvest earnings back into the business for growth, infrastructure, salaries, or operations those retained earnings are taxed at 0%. When you eventually choose to distribute dividends, the standard rate applies at that point. This is a deliberate national policy, not a loophole, and it is one of the reasons Estonia has become a major hub for European tech and e-commerce companies. You can verify the details directly on the official e-Residency portal.

My offshore company already has a payment processor. Should I be worried?

It depends on who that processor is and how they are processing your transactions. If you went through a regulated bank with full underwriting, your risk is lower, though cross-border fees and approval rates are likely still hurting you. If you went through an aggregator or intermediary that promised fast approvals without asking many questions, the risk is real. These relationships tend to end without warning, and the funds held during the freeze period can amount to weeks or months of revenue. Auditing your current processing setup before it becomes a crisis is always the right move. You can start that conversation with us at ireowo.com/preapp.